The prevalence of chronic illnesses and the growing demand for clinical trials are predicted to fuel the market for clinical trial matching software during the anticipated time frame. Market participants are focusing more on new features and creating innovative products due to supportive government initiatives and swiftly advancing technology. Additionally, the healthcare industry is also growing as a result of the quick rise in the number of businesses offering novel customizable features. Clinical trial software is predicted to grow in importance in the future, driving the global market for clinical trial matching software throughout the forecast period due to the increasing demand for remote monitoring services and digitally connected platforms.

COVID-19 IMPACT

The COVID-19 epidemic is a remarkable worldwide public health disaster that has affected most industries, and long-term effects are anticipated to impede industrial growth in the next years. Numerous clinical studies aiming at bringing new therapies to market have been severely hampered by COVID-19, wrecking havoc on international markets. The situation has worsened as a result of labor shortages, supply chain disruptions, and other limitations. Limitations and boundaries have had an impact on a number of ongoing clinical research investigations in many therapy fields. Clinical research teams have developed a new COVID-19 vaccination to combat the problematic condition.

DRIVING FACTORS

Growing Clinical Trial Activity is Anticipated to Fuel Market Expansion

It is anticipated that rising clinical trial activity will fuel the market for clinical trials matching software. Over the past few decades, there had been a tremendous increase in clinical studies. This is a result of the increased penetration of cutting-edge medical technology and the rising desire for novel medications with higher efficacy. But because clinical trials are designed to gather and organize data that can be shared with several healthcare practitioners and disseminated across multiple systems, a clinical trial matching system is quick and inexpensive. The monitoring and tracing of patient registrations and databases, as well as location identification and recruitment, can all be aided by this technology.

RESTRAINING FACTORS

Market's Expansion is Being Hampered by the High Cost of Matching Software

The high cost of matching systems is constraining the market expansion of clinical trial matching software. Initialization, contractual term commitment, per user, per study, training, support and maintenance, validation/21 part 11 compliance, and system integration fees collectively increase the entire cost necessary for clinical trial matching software solutions deployment. Setup fees apply to both on-premises and SaaS solutions. Companies are assessed additional configuration and modification fees following their unique organizational and research needs. Different cost structures are seen depending on the number of users and sites taken into consideration.

SEGMENTATION

By Component

Based on components, the clinical trials matching software market is segmented into services and software. The software category dominated the market in 2021. High utilization and greater medication trial adoption support this segment's growth. Complex medication trials are being encouraged by numerous biotech, pharmaceutical, and clinical research organization corporations.

By End-User

By end-user, the market is segmented into clinical research organizations (CRO), pharmaceutical and biotechnology companies, and medical device firms. The pharmaceutical and biotechnology companies category dominated the market in 2021 due to the numerous clinical trials needed for product introductions. The market is divided into pharmaceutical and biotechnology companies, CROs, and medical device companies based on end-use.

By Deployment Mode

By deployment mode, the market is segmented into on-premise and web & cloud-based. The web & cloud-based category dominated the market in 2021 due to the cloud computing architecture, which is simpler to run and requires no ongoing maintenance. Development costs are decreased because a company's server infrastructure is not needed. The integration time is much shortened, and it is accessible from anywhere. Data sharing is practical and enables teamwork on many projects.

REGIONAL INSIGHTS

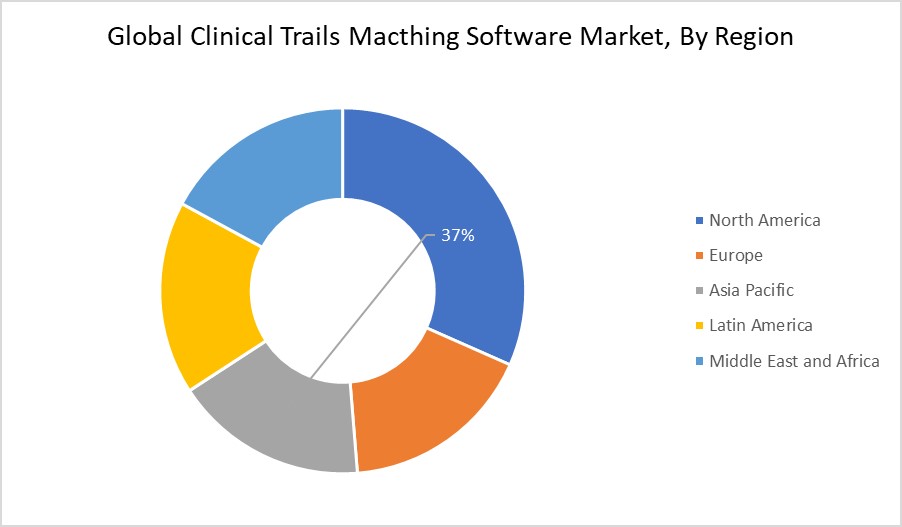

North America is projected to hold the largest clinical trials matching software market share over the forecast period. The introduction of drug trial matching systems by American pharmaceutical and biotechnology businesses is credited with the growth. Additionally, the encouraging government IT initiatives and the growing use of patient matching and clinical trial matching software are contributing to the expansion of this industry.

On the other hand, the Asia Pacific clinical trials matching software market is anticipated to grow significantly over the forecast period due to the region's accessibility to a high number of patients. Many businesses want to locate their research and development operations in Asia Pacific, contributing to the local market expansion. This expansion is explained by an increase in healthcare IT initiatives, a booming economy, and a general improvement in the healthcare infrastructure, particularly in developing nations like China and India.

LIST OF KEY COMPANIES PROFILED:

- Advarra

- Antidote Technologies, Inc.

- IBM Clinical Development

- Clinical Trials Mobile Application

- SSS International Clinical Research

- Aris Global

- Clario

- Bsi Business Systems Integration AG

- Microsoft Corporation

- Ofni Systems

KEY INDUSTRY DEVELOPMENTS:

- July 2022: The Advarra Cloud solution facilitates end-to-end integration and automated, frictionless research document exchange between sites, sponsors, and CROs. It was created in collaboration with Advarra's Site-Sponsor Consortium.

| Attributes | Details |

| Study Period | 2016-2028 |

| Base Year | 2021 |

| Estimated Year | 2022 |

| Forecast Period | 2022-2028 |

| Historical Period | 2016-2020 |

| Unit | Revenue (USD Million) and Volume (Kilo Tons) |

| Segmentation | By Components, By End-User, By Deployment Mode and By Geography |

| By Component |

|

| By End User |

|

| By Deployement Mode |

|

| By Region |

|